Insurance: Common Property -Strata & Community Title

Strata & Community Corporations must insure all common property

A Strata Corporation was underinsured by approximately 75%. A major loss by a gas explosion in the basement caused so much damage that it exceeded the total sum insured. This meant that all owners personally paid many $10,000s to make up the shortfall in the insurance payout. Under the Strata Titles Act, all owners are jointly and severally liable for any shortfall.

Legislation – Strata Titles Act

Click on Legislation above, to view strata title legislation and hints.

Legislation – Community Titles Act

Click on Legislation above, to view community title legislation and hints.

Link to CHU Underwriting Agencies site Policy Documents for policy wording and a definition of ‘Insured Property’.

Prescribed Events: The Insurance Contracts Act 1984 (regulations) includes in its prescribed events

- fire or explosion

- lightning or thunderbolt

- earthquake

- housebreaking, theft, or an attempt to commit theft or burglary

- a deliberate or intentional act

- bursting, leaking, discharging or overflowing of fixed apparatus, fixed tanks or fixed pipes used to hold or carry liquid of any kind

- impact by or arising out of the use of a vehicle (including an aircraft or waterborne craft).

Improvements: The Corporation and/or its owners may undertake improvements to the buildings and common property. e.g. bedroom built-ins, a Corporation BBQ, pergolas or owners upgraded kitchens and bathrooms. These improvements need to be insured. Owners, therefore, must advise the Corporation of any substantial works undertaken in their units. The Corporation must keep the insurance company informed of any changes to the common property or to individual units.

One insurer provides an automatic increase in cover for lot/unit owners fixtures and fittings where the Corporation is not aware of the increase in the replacement value of the building.

Replacement value: This not only covers the cost of rebuilding but must also include the cost of demolition, council and engineering costs amongst other charges. This value excludes the land cost, that is, it is not related to the selling or real estate value of the units.

Hint

Don’t rely on any increase your insurance company suggests. This is no substitute for a valuation.

Best Practice

Valuations: It is strongly recommended that all Corporations obtain a professional replacement valuation at least every 5 years. If your group refuses to do so we recommend that this refusal be noted in the meeting minutes, this might include the names of those in favour and those against. In this case, if a group is underinsured, you have done your best to alert them to the need for a valuation. By doing this, the owners voting against the proposal have knowingly accepted liability.

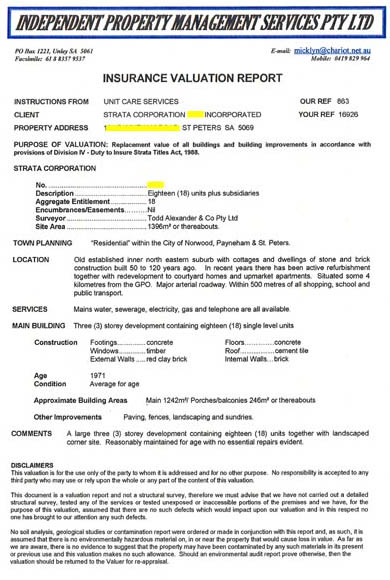

The following is an example of a professional valuation for a strata corporation. It was undertaken by a qualified valuer and it is based on the cost to replace the group. (click on the images below to enlarge)

In this case, the valuer visited the property and inspected a representative sample of the units. The valuation includes: Main buildings, Carports/Garages, Improvements, Demolition costs, Council & Architect fees and GST (Goods & Services Tax).

We use and recommend Michael Hadley & Associates 0419-829-964

Note: Under the Strata & Community Titles Acts all owners are jointly and severally liable for any shortfall in the common property building sum insured, when reinstating the building(s).

If a manager or officer fails to alert owners to the need for a valuation, or is aware that the group is insured well below the average expected, then the Corporation and its officers may be considered negligent.

In professionally managed groups owners rely on their manager for sound advice, with the expectation that they will look after their best interests at all times.

Strata Titles Act (plan number less than 20,000)

Building Insurance: What does the Strata Titles Act require?

Section 30 of the Strata Titles Act spells out the insurance related responsibilities of a Strata Corporation.

Section 30: Insurance

(1) A strata corporation must keep all buildings and building improvements on the site insured to their replacement value.

(2) The replacement value of buildings and building improvements is the cost of their complete replacement including the cost of any necessary preliminary demolition work, any necessary surveying, architectural or engineering work and any other associated or incidental costs.

(3) The insurance must be against –

(a) risks of damage caused by events (other than subsidence) declared to be prescribed events in relation to home building insurance under Part 5 of the Insurance Contracts Act 1984 of the Commonwealth; and

(b) risks against which insurance is required by the regulations.

(4) Any money to which a strata corporation is entitled under a contract of insurance in relation to damage to buildings or building improvements must, subject to any contrary order of the Court, be applied by it in reinstating or repairing those buildings or building improvements.

What does this mean?

Buildings: All common property buildings must be insured, this includes:

- the walls and floors (excluding the owner’s contents)

- the boundary fences, including those between the units

- roads

- the electricity, water supply and sewer

- the inside of units including the owner’s walls

- all of the fixtures and fittings inside the units such as: kitchen cabinets, tap ware and benches, fixed air conditioners which are considered to be part of the building.

Community Titles Act

Building Insurance: What does the Community Titles Act require?

Section 103 & 104 of the Community Titles Act spells out the insurance related responsibilities of a Community Corporation.

103—Insurance of buildings etc by community corporation

(1) A community corporation must insure—

(a) the buildings and other improvements (if any) on the common property; and

(b) in the case of a strata scheme—the building or buildings divided by the strata plan. Maximum penalty: $15 000.(2) The insurance—

(a) must be against risks that a normally prudent person would insure against and risks that are prescribed by regulation; and

(b) must be for the full cost of replacing the buildings or improvements with new materials; and

(c) must cover incidental costs such as demolition, site clearance and architect’s fees.(3) In the event of a claim, any excess or shortfall resulting from under insurance must be met by the corporation.

104—Other insurance by community corporation

(1) A community corporation must insure itself—

(a) against risks that a normally prudent person would insure against; and

(b) against such other risks as are prescribed by regulation. Maximum penalty: $15 000.(2) The amount of the insurance must be the amount that a normally prudent person would insure for but in the case of bodily injury must be at least ten million dollars or such greater amount as is prescribed by regulation.

What does this mean?

Strata Division – one lot above another

Buildings on community titled Strata Divisions are treated the same as a Strata Titled group. The corporation owns the buildings..

Buildings: All common property buildings must be insured, this includes:

- the walls and floors (excluding the owner’s contents)

- the boundary fences, including those between the units

- roads

- the electricity, water supply and sewer

- the inside of units including the owner’s walls

- all of the fixtures and fittings inside the units such as: kitchen cabinets, tap ware and benches, fixed air conditioners which are considered to be part of the building.

For regular lot by lot Community Corporations each lot owner owns all buildings on their respective lots and therefore their insurance. If a wall is shared (party wall), such as with a townhouse, the two lot owners share ownership and a duty to insure.

Hint

Check the By Laws as they often mention insurance.

Some lot by lot (non strata division) groups save considerable money by insuring collectively.